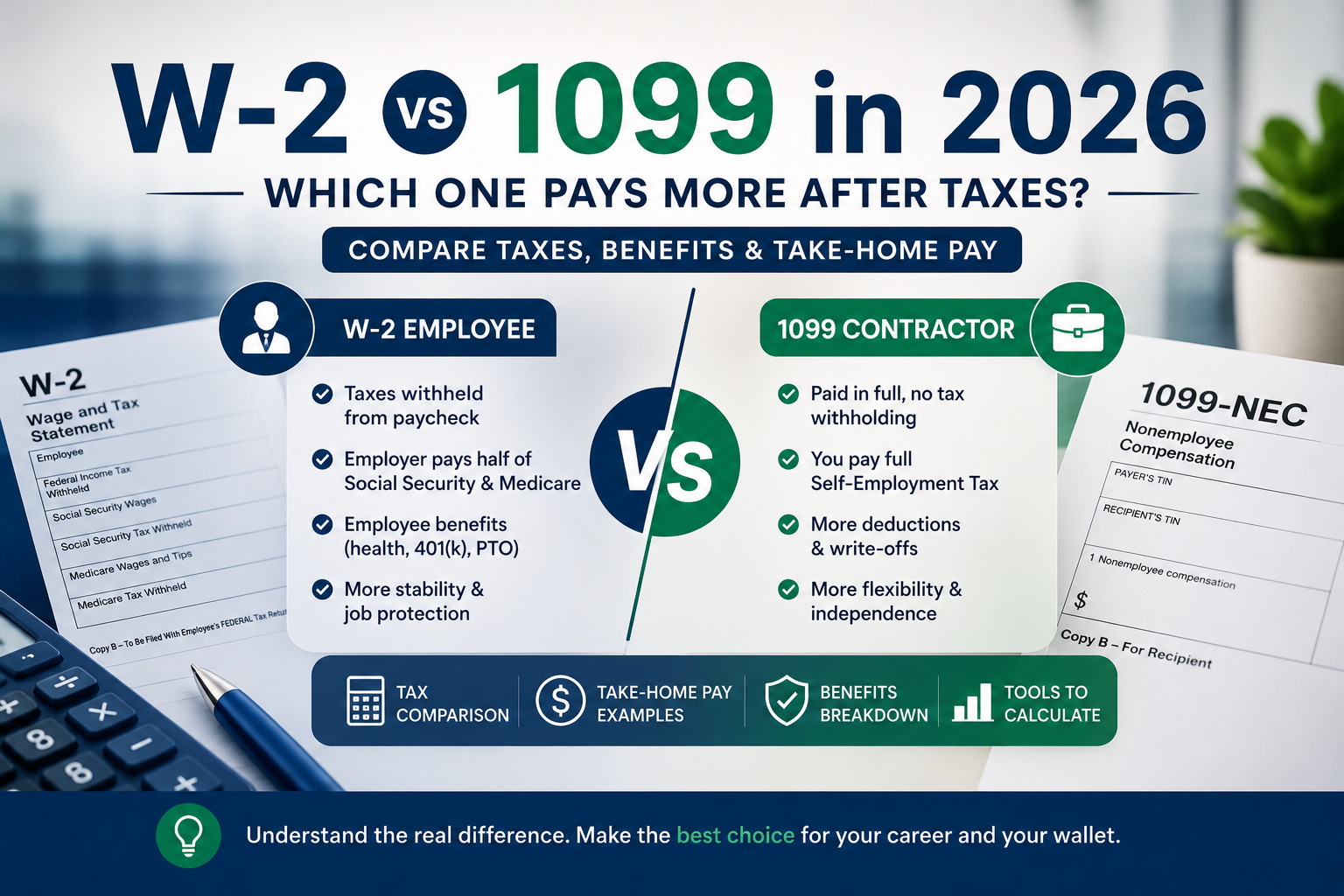

W-2 vs 1099 in 2026: Which One Pays More After Taxes?

Quick Answer

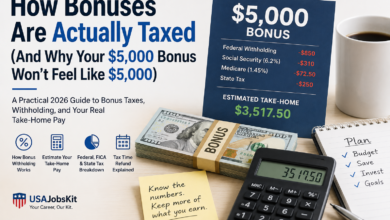

W-2 workers are employees. Taxes are withheld from each paycheck, and employers usually cover part of Social Security, Medicare, and benefits. 1099 workers are independent contractors. They receive gross pay, pay the full self-employment tax on their own, and buy their own benefits. A higher 1099 rate does not always mean more take-home pay once you factor in taxes and benefits. If you want a quick estimate, start with the W-2 vs 1099 calculator.

If you have ever wondered whether it is better to be paid on a W-2 or a 1099, you are really asking about three things: taxes, benefits, and risk. The gross number on a contract is only part of the story, which is why many workers also compare the numbers with a take-home pay calculator before making a decision.

In this guide, you will see the practical differences between W-2 and 1099 in 2026, how each status affects your paycheck, and how to compare offers using tools like a paycheck calculator and a self-employment tax calculator.

Quick overview: W-2 vs 1099

| Factor | W-2 employee | 1099 contractor |

|---|---|---|

| How you are paid | Regular payroll with taxes withheld | Paid in full per invoice, project, or schedule |

| Tax forms | Receive Form W-2 each year | Usually receive Form 1099-NEC if paid $600+ by a client |

| Payroll taxes | Social Security and Medicare split between employer and employee | Pay full self-employment tax on net earnings |

| Benefits | Often eligible for employer benefits and protections | Typically responsible for own insurance and retirement |

| Typical use | Ongoing role, part of the team | Project-based, specialized, or flexible work |

The IRS, state agencies, and courts look at factors such as control, financial risk, and relationship length when deciding whether a worker should be treated as an employee or an independent contractor. It is not just a matter of which tax form you prefer, and it also affects how you should estimate your take-home pay.

What being W-2 means

As a W-2 worker, you are an employee. You fill out Form W-4 when you start the job, and your employer uses that to withhold income tax and payroll taxes from each paycheck. If you are new to paycheck math, it helps to review how a paycheck calculator estimates deductions.

Key features of W-2 work

- Your employer withholds federal income tax, Social Security, Medicare, and usually state and local tax if they apply.

- You receive a regular paycheck on a schedule, such as weekly, biweekly, semimonthly, or monthly.

- You may be eligible for benefits such as health insurance, retirement plans, paid time off, and other perks.

- You are covered by many employment protections such as minimum wage and overtime rules in most situations.

The cost of these benefits is not always obvious, but they can be a big part of your total compensation. That is why comparing a W-2 salary with a 1099 rate requires more than just the hourly number, and why a net pay calculator can be useful when you want a cleaner after-tax comparison.

What being 1099 means

As a 1099 worker, you are usually treated as an independent contractor. Clients pay you in full, and you are responsible for setting money aside for taxes and filing estimated payments. If you freelance or invoice clients directly, the self-employment tax calculator is usually one of the first tools to check.

Key features of 1099 work

- Clients do not withhold income tax or payroll taxes from your payments.

- You often invoice per project or per hour, with a rate that may be higher than an equivalent W-2 wage.

- You handle your own quarterly estimated taxes and self-employment tax on net earnings.

- You usually buy your own health coverage and set up your own retirement savings plans.

This extra control can be attractive, but it also means you carry more tax and financial responsibility. Self-employment tax alone can surprise new contractors who move from W-2 to 1099 without planning ahead, which is why many people compare contractor earnings with a gross to net calculator as well.

How taxes work: W-2 vs 1099

For W-2 employees

- Employers withhold federal and often state income taxes based on your W-4.

- Employers and employees split Social Security and Medicare taxes. Each side generally pays the same rate on wages, up to applicable wage bases.

- You get a Form W-2 that shows wages and tax withheld, and you use that to file your tax return.

If you want to estimate what actually hits your bank account from employee wages, the easiest tool is usually the take-home pay calculator.

For 1099 contractors

- No tax is withheld from payments. You usually make quarterly estimated payments instead.

- You pay the combined Social Security and Medicare rate through self-employment tax on your net earnings.

- You receive one or more Forms 1099-NEC if you are paid at least $600 by a client during the year.

That means the same income can feel very different in your bank account depending on whether you are W-2 or 1099. If you are trying to compare them side by side, combine a paycheck calculator with a self-employment tax calculator instead of guessing.

Which one pays more after taxes?

There is no single correct answer. Some 1099 contracts pay enough to offset the extra tax and benefits you cover yourself. In other cases, a W-2 job with strong benefits ends up being more valuable even if the salary looks lower on paper.

Good rule of thumb: Put both options on the same after-tax basis. Compare estimated take-home pay plus the value of benefits, not just the top-line rate.

To do that, use the right comparison tools instead of rough mental math:

- Use the W-2 vs 1099 calculator to compare net income from each type of work.

- Use the paycheck calculator to estimate W-2 take-home pay.

- Use the self-employment tax calculator to estimate contractor tax on net earnings.

- Use the salary calculator if you need to convert annual, monthly, biweekly, weekly, daily, or hourly pay first.

Example: W-2 job vs 1099 contract

Scenario: Same gross pay, different status

Imagine you can earn $70,000 as a W-2 employee or $70,000 as a 1099 contractor for similar work. The gross number is the same, but the details are not.

- On the W-2 side, the employer pays part of Social Security and Medicare, often offers benefits, and you see tax withholding show up on each paycheck.

- On the 1099 side, you pay the combined self-employment tax on your net earnings and usually need to buy your own health coverage and fund your own retirement.

Instead of assuming the 1099 option is better because it feels more flexible, run both through the W-2 vs 1099 calculator and compare take-home pay and benefits side by side.

Common mistakes when thinking about W-2 vs 1099

- Focusing only on the hourly rate or day rate. A higher contract rate does not help if taxes and benefits eat up the difference.

- Ignoring self-employment tax. New contractors sometimes forget that they are paying both sides of Social Security and Medicare through self-employment tax.

- Assuming you can pick your own status. Classification depends on the actual work relationship, not just preference.

- Not budgeting for benefits. Health insurance, time off, and retirement savings still matter even if they are not on a pay stub.

- Comparing offers without a calculator. Rough mental math can miss thousands of dollars in tax and benefits differences.

If you are deciding between job offers, it may also help to read how to calculate take-home pay so you can understand how deductions affect both options.

FAQ: W-2 vs 1099 in 2026

What is the main difference between W-2 and 1099?

W-2 workers are employees on payroll. Their employer withholds income and payroll taxes and typically offers benefits and protections. 1099 workers are independent contractors. Clients pay them in full, and they are responsible for estimated taxes and self-employment tax.

Does W-2 or 1099 usually pay more after taxes?

Contractor rates are often higher per hour, but 1099 workers pay the full self-employment tax on net earnings and usually cover their own benefits. A W-2 offer with good benefits can sometimes match or beat a 1099 rate once you look at total after-tax value.

Which tax forms do W-2 and 1099 workers get?

Employees get Form W-2, which shows their wages and taxes withheld for the year. Contractors commonly receive Form 1099-NEC from each client that paid them at least $600 in a year.

Who pays Social Security and Medicare taxes on W-2 vs 1099 income?

For W-2 employees, employers and employees share these payroll taxes. For 1099 workers, the combined amount is paid as self-employment tax on the tax return.

Can I choose whether I am W-2 or 1099?

Classification depends on how the work is done, how much control the business has, and other factors set by tax and labor rules. Both workers and businesses can face issues if a relationship is classified in a way that does not match the actual facts.

How can I compare a W-2 offer with a 1099 contract?

The most practical way is to estimate take-home pay and then account for benefits. A paycheck calculator can help with the W-2 side, and a self-employment tax calculator can help with the 1099 side. Once both are on an after-tax basis, the comparison is clearer.

Final takeaway

W-2 and 1099 are more than just two different tax forms. They shape how your pay is taxed, which benefits you get, and how much risk you carry in your work life.

Before you say yes to a job or a contract, take a moment to compare both options on an after-tax, after-benefit basis. The right choice depends on your income level, your health coverage needs, your tolerance for variable income, and your career goals.

Compare W-2 and 1099 with real numbers

Use free tools on USAJobsKit to estimate take-home pay and self-employment tax before you decide.

Disclaimer: This article is for general educational purposes and is not tax, legal, or employment advice. Worker classification and tax outcomes depend on your specific facts and current law. For personal guidance, speak with a qualified tax professional or employment advisor.